Financing Strategies

Subway's Acquisition Through Innovative Whole-Business Securitization

The Subway Acquisition

In a move that underscores evolving financing strategies, Roark Capital Partners is to acquire Subway for a staggering $9.55 billion.

Roark Capital's strategic decision to acquire Subway holds profound significance, representing the firm's largest venture to date and positioning it as a formidable contender in the competitive fast food sector. The acquisition is underpinned by Roark Capital's strategic vision of rejuvenating Subway's operations and transforming it into a robust and profitable enterprise.

Notably, the financing structure that accompanies this landmark deal deviates from conventional norms in the restaurant industry, reflecting the innovative prowess of Roark Capital. The funding strategy melds the firm's internal resources with borrowed capital, manifesting a comprehensive approach that reflects the company's financial sophistication.

Roark Capital Partners previous Deals

A few notable acquisitions by Roark Capital Partners and how they were structured:

Arby's Restaurant Group: Roark Capital acquired Arby's Restaurant Group in 2011. The deal was structured as a leveraged buyout (LBO), where Roark Capital used a combination of its own funds and borrowed money to acquire a controlling stake in Arby's. The acquisition aimed to enhance Arby's operations and strengthen its market position within the fast-food industry.

CKE Restaurants (Carl's Jr. and Hardee's): Roark Capital acquired CKE Restaurants, the parent company of Carl's Jr. and Hardee's, in 2013. Roark Capital's investment allowed CKE Restaurants to focus on expanding its footprint and improving operational efficiency.

Anytime Fitness: In 2014, Roark Capital acquired Anytime Fitness, a global gym franchise. This acquisition demonstrated Roark Capital's interest in the fitness and wellness sector, outside of restaurant industry.

Drybar: Roark Capital invested in Drybar, a blowout salon chain, in 2017, perhaps as growth equity investment, with minority stake. Roark Capital's investment supported Drybar's expansion and brand development.

Jimmy John's: Roark Capital acquired a majority stake in Jimmy John's, a sandwich restaurant chain, in 2019, with aim to drive growth and innovation for the brand.

The Role of Whole-Business Securitization

To facilitate this, Roark Capital has successfully secured $4.9 billion in interim financing from a consortium of banks. This temporary funding is projected to metamorphose into a $5 billion whole-business securitization arrangement, heralding a pioneering paradigm shift in asset-based financing in the restaurant sector. This financial maneuver marks an unprecedented feat, as it would represent one of the largest whole-business securitization deals.

Diving into the intricacies of whole-business securitization reveals a novel approach that holds the potential to redefine corporate funding landscapes. By leveraging this technique, corporations can offload specific assets, such as accounts receivable, to a specialized entity known as a special purpose vehicle (SPV). Subsequently, the SPV issues debt securities to prospective investors, anchoring them with the very assets in question. This ingenious mechanism empowers companies to amass capital without incurring additional debt, fostering financial agility and resilience.

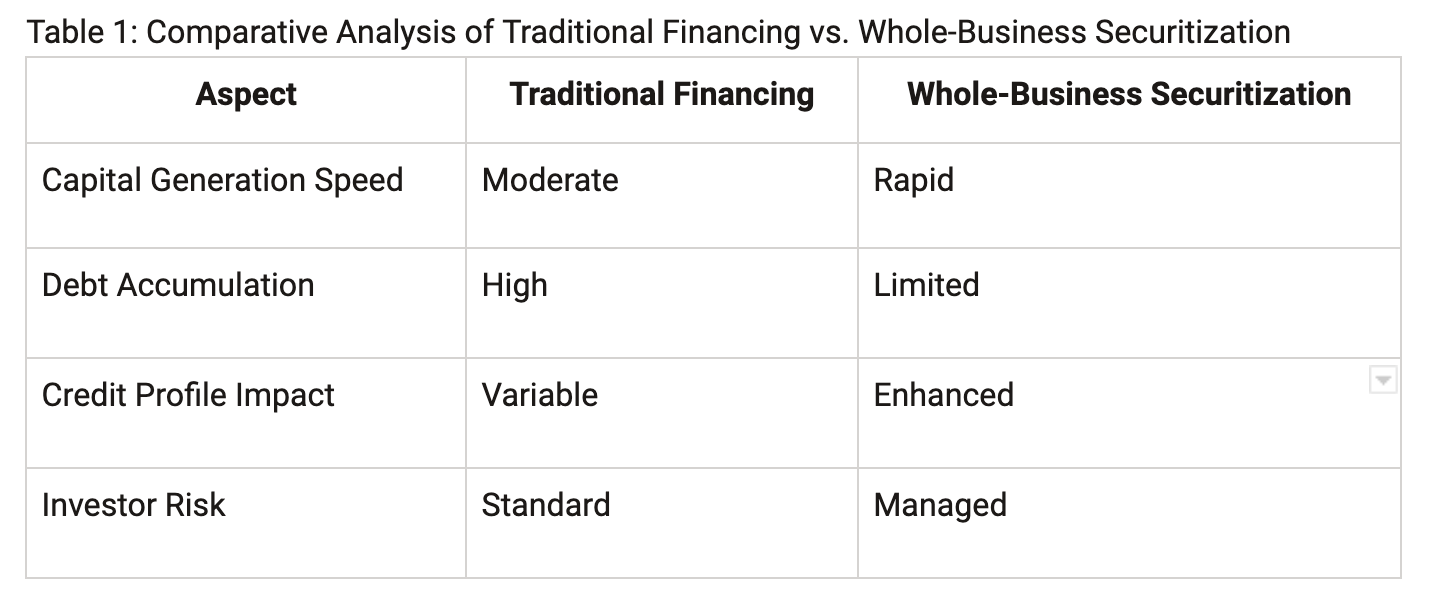

Let’s do a quick comparison of how traditional financing compares with whole-business securitization.

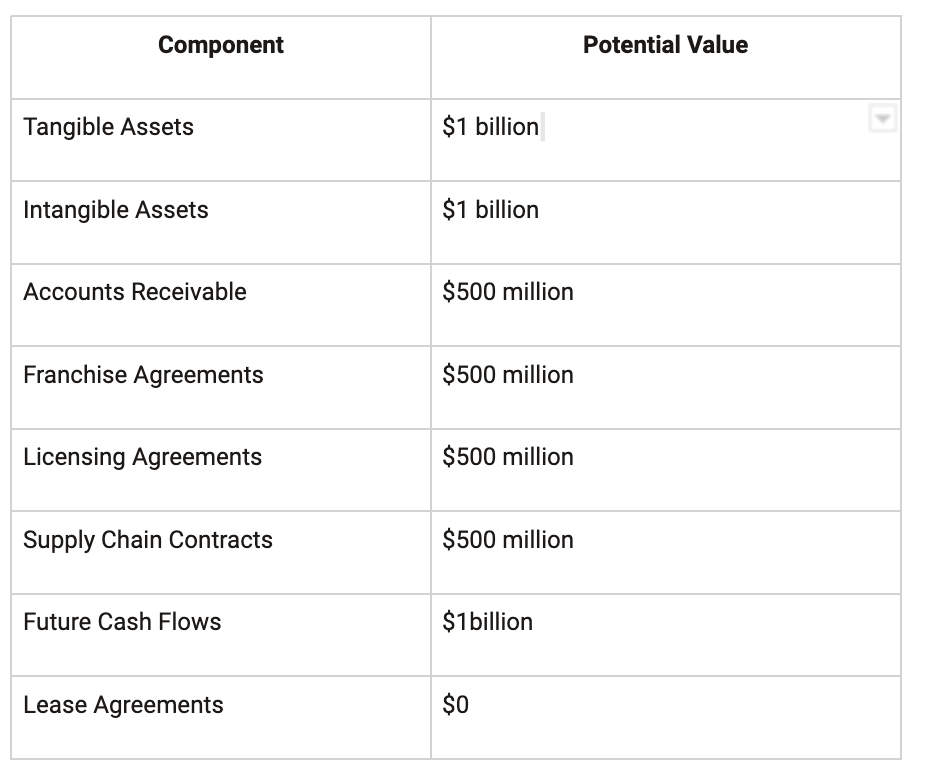

Here is an example breakdown of what a Whole-Business Securitization could include. These are example numbers and not what is included in the Subway deal, because Subway is private company and there is not much public information available.

Table 2: Components Included in Whole-Business Securitization

Tangible Assets: These include physical assets such as real estate, equipment, and inventory. The value of tangible assets can range from millions to billions of dollars, depending on the size and scope of the business.

Intangible Assets: Intangible assets encompass intellectual property, brand value, trademarks, patents, and customer relationships. These assets can hold significant value, often accounting for a substantial portion of a company's overall worth.

Accounts Receivable: The value of outstanding payments owed to the company by its customers. The value of accounts receivable can fluctuate based on sales volume and payment terms.

Franchise Agreements: If the company operates on a franchise model, the rights and agreements associated with each franchise can be securitized. The value would depend on the number and financial health of the franchises.

Licensing Agreements: Similar to franchise agreements, licensing agreements for intellectual property can hold considerable value. This value depends on the popularity and market demand for the licensed content.

Supply Chain Contracts: Contracts with suppliers and vendors can be securitized, especially if they involve long-term agreements or exclusivity clauses. The value would depend on the terms and the stability of the supply chain.

Future Cash Flows: Anticipated future revenues generated by the business can also be securitized. The value is calculated based on projected financial performance and growth potential.

Lease Agreements: If the company leases its properties or equipment, these contracts can be included. The value would be derived from the remaining lease payments.

Advantages and Considerations

The adoption of whole-business securitization in the context of the Subway acquisition is emblematic of its growing prominence as a preferred financing avenue. This trend is underscored by several compelling advantages that this strategy affords:

Expedited Capital Generation: The method expedites the accumulation of substantial capital reserves, enabling companies to swiftly execute strategic initiatives.

Preserved Business Investments: Corporations can retain their internal capital reservoirs, thereby fortifying their core operations and facilitating ongoing innovation.

Enhanced Credit Profile: Through this method, enterprises can enhance their creditworthiness, thereby attaining more favorable borrowing terms in the future.

Debt Alleviation: By harnessing the benefits of whole-business securitization, firms can judiciously manage their debt load, nurturing a more sustainable financial ecosystem.

It is crucial, however, to recognize the associated risks when embarking on such innovative financing pathways:

Asset Performance: If the securitized assets do not yield the projected returns, the SPV might default on its debt obligations, potentially translating into investor losses.

Credit Consequences: The application of whole-business securitization could potentially cast a shadow on the company's credit rating, influencing future borrowing potential.

In essence, whole-business securitization signifies an ingenious yet venturesome financing approach that can yield significant rewards while necessitating careful risk management.

Glimpse into the Future

The Subway acquisition and Roark Capital's innovative financing approach shed light on the growing prominence of whole-business securitization. As this strategy gains traction, we look forward to seeing its potential adoption by forward-looking enterprises across industries.